i9 Intelligence vs. Tracker I-9 (Mitratech): Remote Verification and Pricing Compared

Read the article

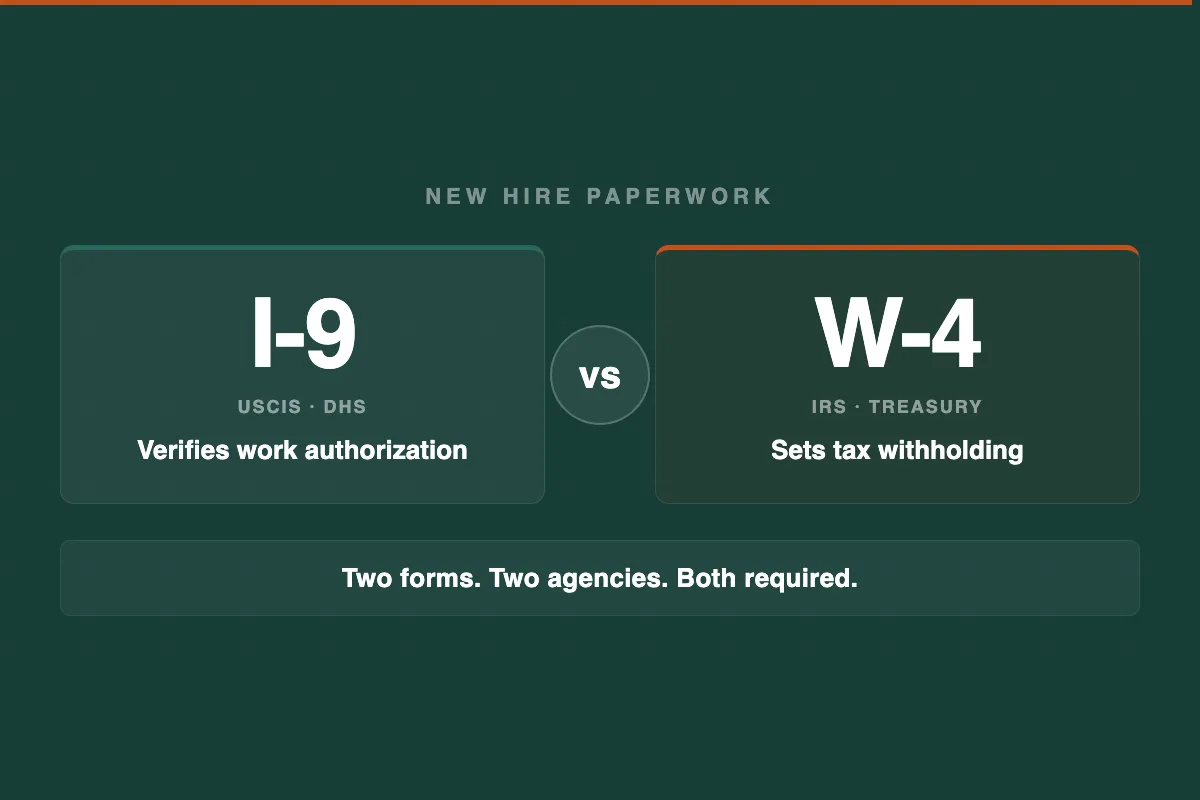

Form I-9 and Form W-4 are two different federal forms that every new employee completes — but they serve completely different purposes. If you're an employer, HR manager, or office manager trying to figure out what paperwork a new hire needs to fill out on day one, here's the short answer on the i9 vs W-4 question: Form I-9 verifies that the employee is legally authorized to work in the United States, while Form W-4 tells you how much federal income tax to withhold from their paycheck.

Both forms are required for employees. Neither is optional. Getting either one wrong — or skipping one entirely — creates compliance problems with different federal agencies. Here's what you need to know about each form and how they work together.

Form I-9, Employment Eligibility Verification, is a federal form required under the Immigration Reform and Control Act of 1986 (IRCA). Every employer in the United States must complete a Form I-9 for every person they hire — regardless of citizenship or immigration status. There are no exceptions based on company size, industry, or the employee's birthplace.

Form I-9 verifies two things:

The form has two main sections completed by different parties:

Employees choose which documents to present from the Lists of Acceptable Documents published by U.S. Citizenship and Immigration Services (USCIS). They can present one document from List A (establishes both identity and work authorization, such as a U.S. passport) or a combination of one document from List B (identity only, such as a driver's license) plus one from List C (work authorization only, such as an unrestricted Social Security card).

Employers must retain completed Forms I-9 for 3 years after the date of hire or 1 year after employment ends — whichever is later. If the government requests an inspection, you must produce your I-9 records within 3 business days.

Form W-4, Employee's Withholding Certificate, is an IRS form. Employees complete it so that their employer can withhold the correct amount of federal income tax from each paycheck.

Unlike Form I-9, which is about employment authorization, Form W-4 is entirely about tax withholding. It has no connection to immigration status or work authorization. A W-4 does not verify anything — it simply tells you, as the employer, how much federal income tax to take out of the employee's pay.

Key facts about Form W-4:

Form W-4 only applies to employees (W-2 workers). Independent contractors do not fill out a W-4 — they fill out Form W-9 instead, which is used to collect their taxpayer identification number for 1099 reporting purposes.

| Form I-9 | Form W-4 | |

|---|---|---|

| Purpose | Verify identity and work authorization | Determine correct federal income tax withholding |

| Issuing agency | USCIS (Department of Homeland Security) | IRS (Department of the Treasury) |

| Required for | All employees (no exceptions) | All employees (W-2 workers) |

| Who fills it out | Employee (Section 1) + Employer (Section 2) | Employee only |

| Deadline | Section 1: first day of work. Section 2: within 3 business days of hire. | Before or on first day of work (so withholding can begin correctly) |

| Documents required from employee | Original identity and work authorization documents (List A, or List B + C) | None — employee self-certifies withholding preferences |

| Verifies work authorization | Yes | No |

| Sent to government | No — retained by employer, produced on inspection | No — retained by employer (IRS may request it) |

| Can be updated | Section 1 cannot be amended; corrections follow specific USCIS rules | Yes — employee can submit a new W-4 at any time |

| Enforced by | ICE (U.S. Immigration and Customs Enforcement), DOJ, USCIS | IRS |

Every new employee completes both forms. They are not interchangeable and one does not substitute for the other. Here's how the two forms fit into the onboarding timeline:

Note that Form I-9 requires action from both parties — the employee fills out Section 1, and the employer fills out Section 2 after reviewing the employee's documents. Form W-4, by contrast, is completed entirely by the employee. The employer simply receives it and adjusts payroll withholding accordingly.

The only workers who skip Form I-9 are independent contractors. Contractors are not employees under federal law, so the employment eligibility verification requirement does not apply to them. Instead, contractors fill out Form W-9 (which collects their taxpayer identification number for 1099 reporting). If you're unsure whether someone is an employee or a contractor, err on the side of completing Form I-9 — worker misclassification is a separate and significant liability.

Managing Form I-9 correctly across multiple locations or for remote hires is more complex than most HR teams expect. Schedule a free compliance call with our team, or use our I-9 Risk Calculator to see where your organization stands today.

Employers often think of new hire paperwork as a single stack to hand employees on their first day. That's understandable, but it creates a timing trap with Form I-9. The employee's Section 1 deadline is indeed the first day of work. But the employer's Section 2 obligation has a three-business-day window — not a "get to it whenever" window. Missing the Section 2 deadline is one of the most common I-9 violations.

Unlike Form W-4, which the employee simply fills out and hands over, Form I-9 requires the employer to physically examine original documents. You cannot accept a photocopy, a scan emailed by the employee, or a photo on their phone. The documents must be presented in person — or through a compliant remote verification process using an authorized representative if the employee is hired remotely and participates in E-Verify.

Both Form I-9 and Form W-4 are retained by the employer. Form I-9 is produced for inspection if ICE, the Department of Justice, or the Department of Labor requests it. Form W-4 is retained by the employer and may be requested by the IRS. Neither is proactively filed with any agency at the time of hire.

A common mistake is treating a signed Section 1 as a complete Form I-9. It isn't. The form isn't complete until Section 2 is finished and signed by the employer or authorized representative. Incomplete forms are a paperwork violation even if the employee is fully authorized to work.

Both forms carry penalties for errors, but they come from different federal agencies and operate under different rules.

U.S. Immigration and Customs Enforcement (ICE) can issue civil fines for I-9 paperwork violations — even if every person on your payroll is legally authorized to work. These "technical violations" include missing signatures, incomplete fields, wrong document types accepted, or late completion of Section 2.

Penalties for knowingly hiring or continuing to employ unauthorized workers are substantially higher and escalate with each offense — up to $28,619 per worker for third or subsequent offenses. Criminal penalties are also possible in egregious cases.

Note: I-9 penalty amounts are adjusted annually for inflation under the Federal Civil Penalties Inflation Adjustment Act. The figures above reflect the January 2025 adjustment, which remains in effect through 2026. Always verify current amounts before citing in legal or audit contexts.

If an employer fails to withhold the correct amount of federal income tax because no valid W-4 is on file, the IRS can hold the employer liable for the under-withheld tax. The IRS may also impose a "lock-in letter" that sets a mandatory withholding rate for an employee and cannot be overridden by a new W-4 without IRS permission. Employees who intentionally claim exempt status when they don't qualify can face penalties from the IRS directly.

The practical consequence for employers: if no W-4 is on file, you are required to withhold at the default rate (as if the employee is single with no other adjustments). That protects you from under-withholding liability — but it also means the employee may owe taxes at year-end, which creates friction.

Yes. Every employee (W-2 worker) needs to complete both Form I-9 and Form W-4 at the time of hire. Form I-9 verifies that the employee is authorized to work in the United States. Form W-4 sets their federal income tax withholding. The two forms serve completely different purposes and neither substitutes for the other.

The core difference: Form I-9 is an immigration and employment authorization form administered by USCIS and enforced by ICE. Form W-4 is a tax withholding form administered by the IRS. An employee fills out both on (or before) their first day of work. The employer also completes Section 2 of Form I-9 within 3 business days by examining the employee's documents. The employer uses the W-4 to set payroll withholding but doesn't complete any portion of it themselves.

If an employee doesn't provide a completed W-4, the IRS requires you to withhold federal income tax as if they are single with no adjustments. You cannot hold a paycheck or delay employment over a missing W-4 — just default to the standard withholding rate until the employee submits the form.

No. They cover completely different compliance areas and cannot substitute for each other. Completing one does not satisfy your obligation to complete the other. Both are mandatory for all employees.

Yes. Employees can submit a new W-4 at any time — after a life change like marriage, divorce, a new dependent, or a change in income from a second job. The IRS recommends reviewing withholding annually. Form I-9, by contrast, cannot be changed by resubmission. Any corrections to Form I-9 must follow USCIS correction procedures (draw a line through the error, enter the correct information, initial and date the correction — do not use correction fluid).

Neither, in most cases. Independent contractors are not employees, so they do not complete Form I-9 (employment authorization verification) or Form W-4 (employee tax withholding). Instead, contractors complete Form W-9, which provides their name and taxpayer identification number for 1099 reporting. If you are paying someone as a contractor but the actual working relationship looks more like employment, consult counsel — worker misclassification carries significant liability.

For Form I-9, the employee must present original, unexpired documents from the USCIS Lists of Acceptable Documents — either one List A document (like a U.S. passport) or one List B document (like a driver's license) combined with one List C document (like a Social Security card). For Form W-4, no documents are required — the employee simply fills out the form based on their tax situation and submits it to you.

i9 Intelligence has helped thousands of employers manage Form I-9 compliance across all 50 states. Whether you need help with remote Section 2 verification, I-9 audits, or switching from paper to electronic I-9s, our compliance team is here.